Insights and News

Back to the Future

Dave Weisberger

December 12, 2022

The interesting thing about history is how fast people forget it’s messages. Yesterday, for example, headline CPI posted at 7.5%, a level last seen in 1982 as it was headed down from a peak of over 14%. At that time, the federal reserve under Paul Volker, acted to crush inflationary expectations ruthlessly. They raised REAL rates to over 6%, which was 20% interest rates in nominal terms. That policy, of raising interest rates significantly higher than inflation, worked, driving inflation down and setting the stage for the longest bull market in history.

If we are to believe the mainstream media, today’s inflation print of 7.5% will influence the Federal Reserve to act quicker, reminding the media pundits of that time in the early 80s. That narrative suggests that the Fed’s heroic inflation fighting actions will cool speculative excesses and bring inflation back to their “targeted” levels. Incredibly, they think (or fear) the Fed is likely to act as Volker did & are worried that Bitcoin, as an inflation hedge, is unnecessary. What unadulterated nonsense…

Before explaining the massive differences between 2022 and 1982, I should re-iterate that Bitcoin is not an inflation hedge in the traditional sense (yet), but rather has the potential to preserve wealth during fiat monetary inflation (and to generate wealth for those that believe in that outcome and accumulate it early). My argument is simple: IF Bitcoin achieves a critical mass of acceptance as digital gold, it will be at a market cap in excess of golds current value, as gold has underperformed recently. The basic math suggests that such a price target is roughly 15 times higher than today’s value or more (in 2022 dollars). Until then, Bitcoin trades as a probabilistic option on that eventuality. As a result, it is not surprising that Bitcoin is exceptionally volatile and can, for short periods, be highly correlated to other risk assets. Normally, I try to ignore these short term moves when discussing Bitcoin, but the reaction of pudits to the high consumer inflation triggered me to write this rant…

So, getting back to the Federal Reserve, the most important numbers are NEGATIVE 7.25%, which is the REAL overnight rate today and NEGATIVE 6.75%, which would be the REAL overnight rate if they “hawkishly” raised rates 50 basis points in March instead of the 25 currently predicted. Heck, if they tried to “shock and awe” markets with a 1% raise, it would still leave the overnight rate at NEGATIVE 6.5%…

Anyone else see the difference between today’s Fed and the Volker days???

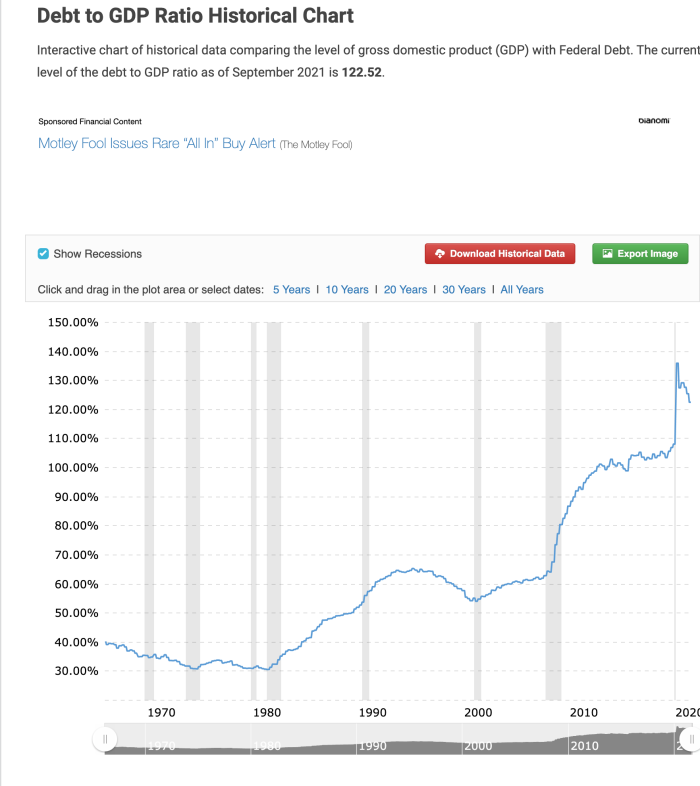

To be clear, I am not advocating for the Volker approach now, but that is because the situation is very, very different. Government debt, as a % of GDP, in 1982, was roughly 34% of GDP, while today it stands at 134%, trending upward. In addition, estimates of the “shadow debt” implied by projected Social Security and Medicare deficits range from double the current debt to much higher than that. The result of this massive increase in debt is that the interest owed to finance it could become untenable. Predictions vary, but most economists agree that debt service, if the yield curve moved much higher, would become so expensive that it could squeeze out ALL discretionary government spending in a balanced budget. With the exception of MMT advocates, who believe that the government never needs to repay their debts, most agree that the government wants to avoid higher interest rates to avoid a crippling increase in their debt service. As a result, they are TRAPPED in a cycle where low interest rates are necessary and inflation to erode the cost of debt is a FEATURE, not a bug…

So, what does this mean for Bitcoin? Simply put, it makes its odds of achieving critical mass much higher, as more people begin to understand the need for a true store-of-value for the digital world. Historically, gold served that purpose, but it is not well suited for a digital economy. In fact, it seems that a transition away from gold is underway as seen by a ratio of its price to the Fed Balance sheet over the past few years:

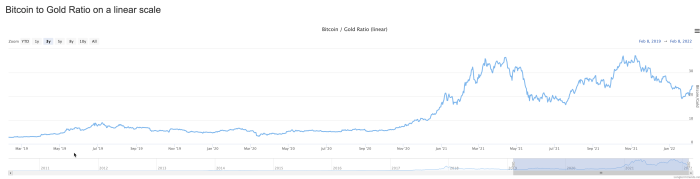

It is likely that many gold buyers, particularly those that bought the metal as a monetary hedge have started to migrate towards Bitcoin on the margin. This trend coincided with the underperformance of gold to the Fed balance sheet shown above, manifesting in Bitcoin outperformance from 2020-mid 2021 as seen below:

Since the initial surge, Bitcoin vs gold has been somewhat rangebound, but, it certainly bears watching. If Bitcoin continues to outperform gold, it could foreshadow a run towards much higher prices. It has to be noted that this is a long term prediction, but, in the short term, the planned rate increases from the Fed might well have a significant impact. If the Fed is able to engineer a collapse in speculative assets, it is almost certain that Bitcoin would drop alongside them. In all likelihood, Bitcoin’s retracement to under $43k this afternoon is directly related to this realization, as it fell in lockstep with Nasdaq’s 2.75% drop. The important takeaway, however, is that such reactions are likely to be short term; as it becomes clear that there is almost zero chance of positive REAL rates from the Federal Reserve. Unless of course, we were able to jump into a DeLorean, hit 88 MPH and have 1.21 gigawats of energy flowing through the flux capacitor to travel back to 1982. Failing that, I suspect that the macro bullish trend for Bitcoin will resume in the not to distant future.